Are you bullish on bearish on HYPE? https://t.co/mEjBjN0HEF

95.2K @seth_fin

95.2K @seth_fin Are you bullish on bearish on HYPE? https://t.co/mEjBjN0HEF

1

1

3

3

2.0K

2.0K

25.9K @trustwalletzh

25.9K @trustwalletzh I'm really feeling numb right now 🥲

Never thought something like this would happen to me

One night five years ago

Under a friend's persuasion

I somehow downloaded @TrustWallet

Since then I couldn't quit, tossing and turning every night, unable to sleep

The moment I close my eyes it's Hyperliquid contracts, bStocks US stock tokens, World Cup prediction market

I just can't resist opening it to take a look

If I don't check it for a day I feel chest tight, anxious, restless

I know regret won't help

Hope everyone learns from my experience

Trust Wallet is truly a "harmful genius" 🥹

0

2

169

11.2K @marilyn100x

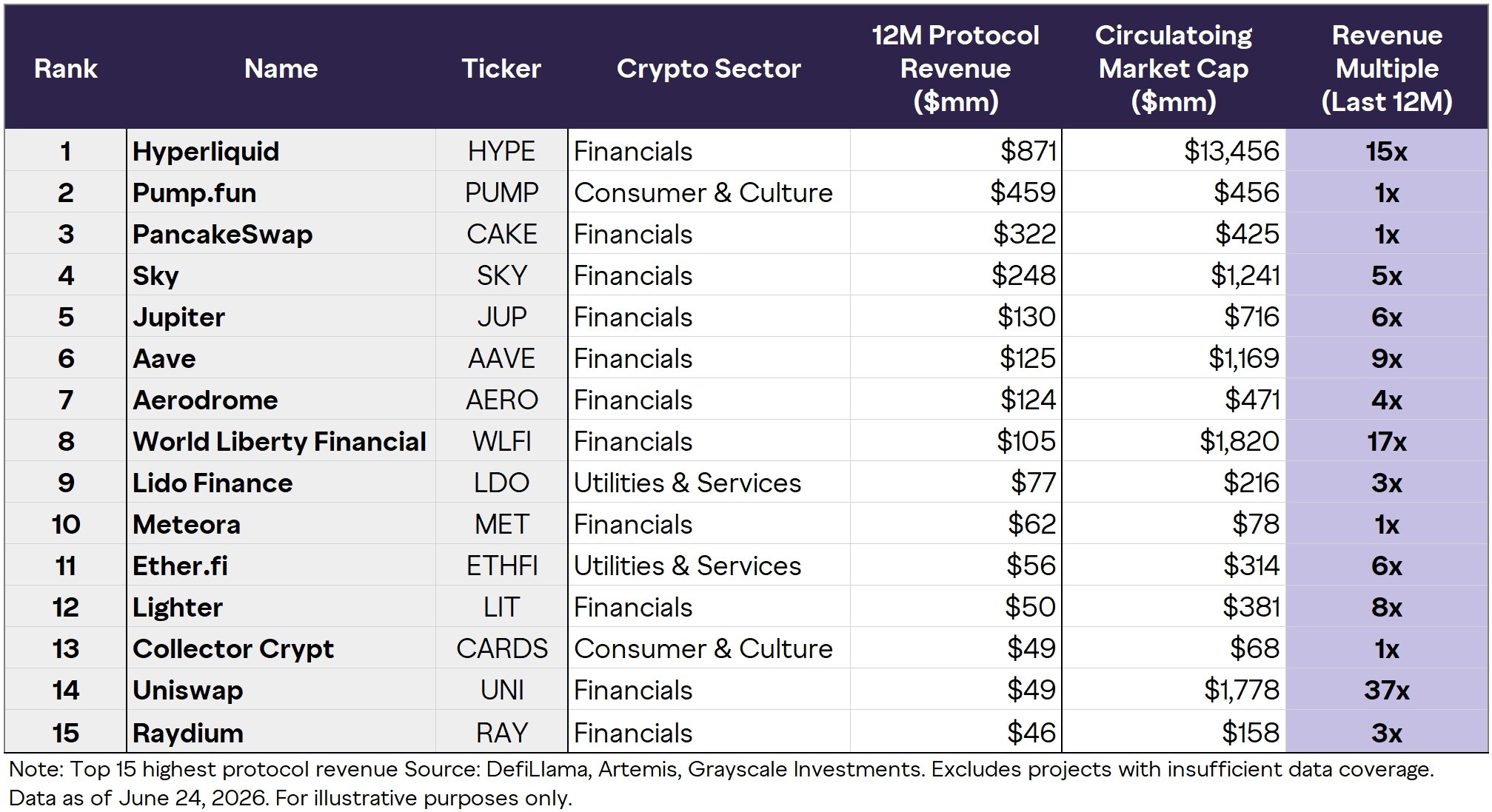

11.2K @marilyn100x 0/ Some of crypto's highest-earning protocols trade at valuations lower than many traditional businesses.

Combined, the top 15 onchain apps generated over $3B in trailing revenue. 12 of those trade below 10x trailing revenue.

Here's what CLARITY Act passage could mean👇 https://t.co/7A6P6zWouW

11.2K @marilyn100x

11.2K @marilyn100x 1/ The revenue is real and it is already running.

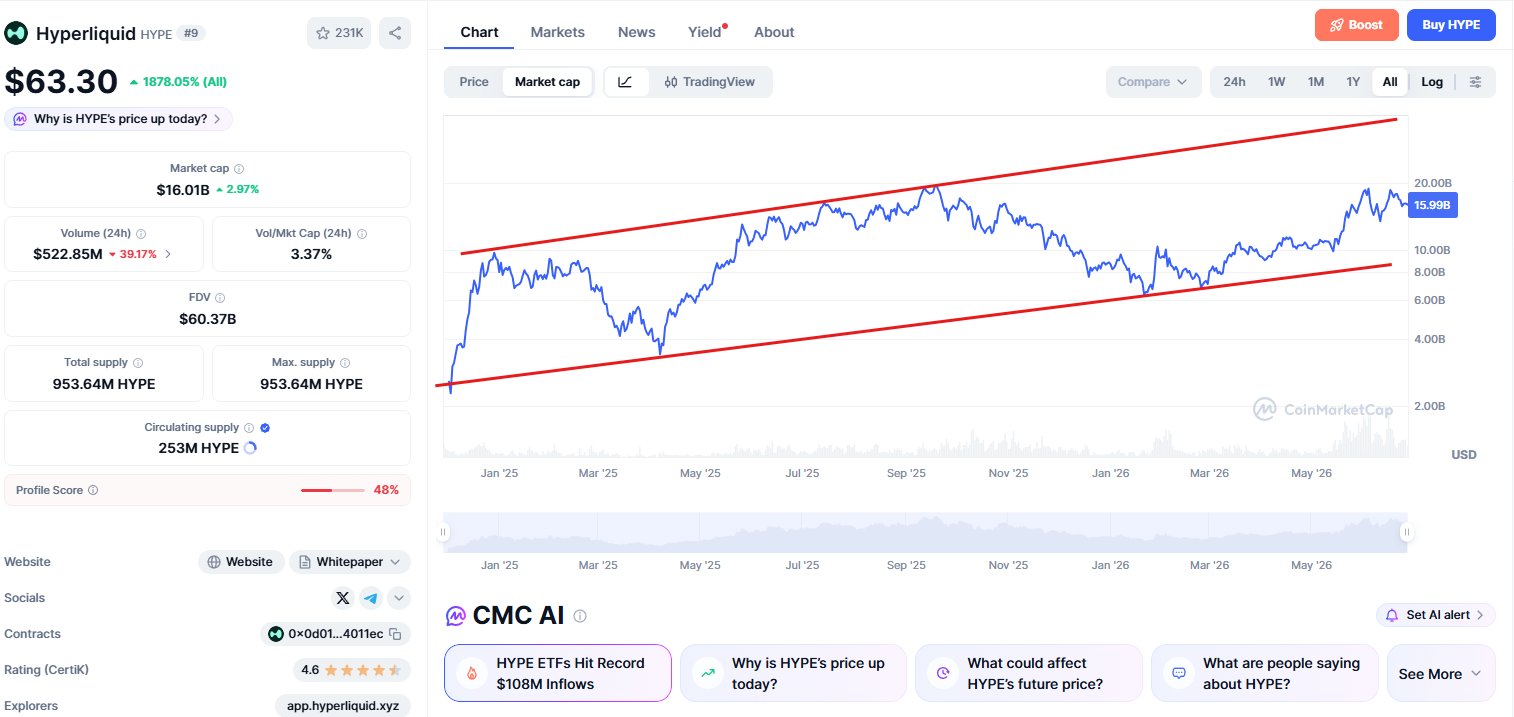

> Hyperliquid: $871M revenue, 15x multiple

> Pumpfun: $459M revenue, 1x multiple

> PancakeSwap: $322M revenue, 1x multiple

> Sky: $248M revenue, 5x multiple

> Aave: $125M revenue, 9x multiple

> Lido: $77M revenue, 3x multiple

> Uniswap: $49M revenue, 37x multiple

The spread runs from 1x to 37x on protocols with comparable order-of-magnitude revenue.

11.2K @marilyn100x 2/ Pumpfun and PancakeSwap sit near 1x despite real revenue. Hyperliquid sits at 15x on a similar scale of revenue.

The simple explanation is durability.

Memecoin and DEX fee revenue decays fast once the next platform launches. Hyperliquid's orderbook and liquidity have held market share for two years straight.

That explains part of the spread. It does not explain Aave at 9x or Uniswap at 37x, both multi-year protocols with real moats.

Institutions need a legal framework before they invest at scale.

A pension fund's compliance team still has to classify what Aave is before it can buy the token. Security, commodity, unregistered exchange. The SEC currently holds discretion to argue any of those positions.

That discretion is a real cost, and it shows up most in the names where durability is not the open question.

11.2K @marilyn100x 3/ CLARITY addresses that specific cost through four provisions.

> CFTC gets exclusive jurisdiction over digital commodity spot markets

> Tokenized financial instruments get the same regulatory treatment as their underlying asset

> Banks get statutory permission to conduct digital asset activities

> DeFi protocols are excluded from intermediary registration requirements

A statute passing does not move pension fund allocations the next quarter. Custody infrastructure, audited financials, and fiduciary sign-off still take years to build.

What changes immediately is the legal answer compliance teams have been waiting on.

11.2K @marilyn100x 4/ Hyperliquid is the complication for this entire thesis.

It trades at 15x without CLARITY having passed.

If the market can already price one protocol's revenue at a real multiple under current legal uncertainty, regulatory clarity is not the only variable standing between revenue and price.

Durability got Hyperliquid there first.

CLARITY is what gives Aave, Uniswap, and Lido the same opening, once the legal question stops being the reason compliance teams cite for waiting.

11.2K @marilyn100x 5/ $3B in combined trailing revenue sits across these 15 protocols today. Some of that revenue is durable, some isn't.

CLARITY does not fix the fragile revenue.

It removes the legal excuse for mispricing the durable kind correctly.

6

2

380